The Ingenesist Simulation

Engineering Productivity and Collective Insurance Pools are the Flywheel of Economic Growth and Decentralized Governance

Further to

the phase space of insurance profitability and sustainability was explored re-incorporating the principles from

And this broadly proving the requirement for

and

in order for decentralized governance to work. The python Jupyter notebook simulation is available on Google Colab. This further confirms Dan Robles’ Ingenesist Project original insights vis a vis insurance, engineering productivity and collective intelligence. The write up was created with Deepseek.

TL;DR for Cypherpunks & Privacy Tech

Opacity alone centralizes power. UNISS‑GX‑SD‑B showed that a pure dark market for secrets ends in 100% capture. No amount of cryptography fixes that.

Insurance pools as a “sink” stop capture – but in the first integrated model, pools always lost money. The sink worked, but it was a charity.

A minimal mandatory baseline subscription (3–5% of agents) turns the sink profitable when paired with engineering knowledge that generates real returns. Safe + profitable runs jumped from 0% to 2.9% of the parameter space.

The Gini coefficient drops dramatically – from ~0.42 in surveilled baselines to ~0.18 in our privacy‑preserving runs. Privacy doesn’t increase inequality; it can reduce it when paired with the right institutions.

Engineering productivity is the flywheel. In the simulations, the single strongest driver of profit was the future income stream from engineering secrets (

eng_productivity_factorcorrelation 0.20). Pools that bought more engineering secrets not only reduced risk but earned a steady return that paid for kompromat purchases. This turns the sink into a self‑sustaining engine: engineers produce value, pools capture it, and that value funds collective defence. Without this productivity loop, even a mandatory fee only stabilises losses; with it, the system can become profitable.Pure insurance is fragile. Voluntary uptake is near zero. You need a collective defence layer – a small, unavoidable fee that funds the permanent buyer. This isn’t a tax; it’s the economic spine of a resilient, self‑governing network.

“Decentralized governance” is usually about voting, not defence. Real decentralisation requires a mechanism to neutralise power‑hoarding. The simulations prove that a designed market with a permanent buyer does that – and it works even when the buyer loses money, but to be sustainable it must have a reliable income stream.

The fractal defence stack (individual → mutual aid → federated → global) maps directly to this economic model. The mandatory fee can be implemented as a smart contract that scales across layers, adaptive and AI‑orchestrated, but the core insight is simple: defence has to come from somewhere, and if we don’t fund it collectively, the system will be captured.

Bottom line: Privacy tech without institutional defence is a vulnerability. Build the sink, fund it with a minimal subscription, and let engineering value creation pay the rest. That’s how you get a decentralised economy that’s both private and anti‑fragile.

Executive Summary: From Privacy to Prosperity – The Economics of Anti‑Capture

A series of agent‑based simulations (UNISS‑GX‑SD) has revealed a fundamental tension in privacy‑preserving systems: total opacity without institutional buyers leads to hoarding, corruption, and systemic capture. When we introduced insurance pools as permanent buyers of secrets (a “sink”), capture was eliminated across 96% of the parameter space—but the pools consistently lost money. This left a gap between the technical possibility of neutrality and the economic reality of sustainability.

In a refined sweep (2000 runs, 5000 steps each), we focused on the most promising region and added a mandatory baseline subscription to model a small, unavoidable fee. The results show that a minimal forced contribution—just 3–5% of agents—coupled with a productive engineering sector, turns the sink into a profitable, self‑sustaining defense system. Key findings:

Zero flips became the majority outcome (59% of runs), confirming that a well‑tuned market can prevent capture even under adverse conditions.

Profitability is now achievable (5% of runs), with strong positive correlation to engineering productivity (

eng_productivity_factor= 0.20) and high initial capital.The mandatory fee acts as a bootstrap, not a tax: safe+profitable runs used only a third of the average mandatory fraction (3.2% vs. 10.2%). A small base income is sufficient; larger fees correlate negatively with profit.

Stability depends on limiting kompromat supply: low

lambda_komp, lowf_hunters, hightheta_sell(hunters sell most secrets), and highflip_thresholdare the strongest predictors of zero flips.

These results reframe the cypherpunk narrative: privacy is necessary but insufficient. A dark market without institutional demand leads to centralization of power—a classic “lemons market” failure. Yet when we pair privacy with a designed market that values both risk reduction (insurance) and value creation (engineering knowledge), the system becomes anti‑fragile. The engineering sector acts as a flywheel: verified knowledge generates returns that fund the removal of harmful secrets.

For academic audiences in political economy, sociology, criminology, and behavioral psychology, the simulation offers a laboratory for institutional design. It shows that:

Capture is not inevitable; it can be structurally neutralized by creating a permanent buyer.

Adverse selection (hunters hoarding high‑potency secrets) does not break the system when pools continuously drain even low‑potency secrets.

Voluntary cooperation emerges from self‑interest: agents choose insurance when it is affordable, and engineers contribute because their work is valued.

Inequality is naturally moderated (Gini <0.2 in many runs), suggesting that privacy‑preserving markets may produce more equitable outcomes than surveilled counterparts.

The simulation is intentionally simplified—a flat mandatory fee. In practice, such a fee could be implemented as a fractal smart contract, mirroring the Darkweave protocol’s vision of security scaling from individual to global. It could be adaptive, governed by on‑chain AI, with rates varying by contribution, threat level, and fractal layer. The core economic insight, however, is universal: a minimal baseline subscription can transform a loss‑making sink into a self‑funding engine of collective security.

This work bridges privacy technology, institutional economics, and behavioral science. It provides a quantitative foundation for designing privacy‑preserving economies that are not only resilient to capture but also economically sustainable. The mathematics now show the path; the next step is to build the infrastructure.

Refined Simulation Results: The Economic Foundation of Fractal Defense

Overview

The initial UNISS‑GX‑SD simulations showed that insurance pools acting as a permanent buyer of secrets (a “sink”) could eliminate systemic capture, but pools consistently lost money due to negligible voluntary insurance uptake. In this follow‑up study, we focused the parameter space on the most promising region identified earlier and introduced a mandatory insurance fraction to model a baseline subscription. The goal was to see whether a small, unavoidable fee could make the sink self‑sustaining while preserving its anti‑capture properties.

We ran 2000 simulations (5000 steps each) with a Latin hypercube design, narrowing ranges to the zone where safe and profitable outcomes were most likely. The results confirm that a minimal mandatory fee, combined with a productive engineering sector, can turn the sink into a profitable, resilient defense system.

Key Findings

Zero flips are now the majority outcome

59.1% of runs had no flips (up from 30% in the initial sweep).

The median number of flips is zero.

This demonstrates that narrowing parameters to the safe region dramatically improves stability.

Profitability remains challenging but is achievable

Only 5% of runs were profitable (positive pool profit), and 2.9% were both safe and profitable.

However, when profitability occurs, it can be substantial (max profit ~4.7 million vs. median loss ~‑4,300).

This suggests a threshold effect: once the right conditions align, the system can become highly profitable.

The mandatory insurance fraction was unexpectedly low in safe+profitable runs

Mean mandatory insurance in safe+profitable runs was 3.2%, compared to 10.2% in other runs.

This indicates that the mandatory fee acts as a bootstrap – a very small forced base is enough to push the system into viability, and beyond a point it may become counterproductive (correlation with profit is negative).

Engineering productivity is the strongest driver of profit

eng_productivity_factorhas the highest positive correlation with profit among non‑automatically‑linked variables (0.20).Safe+profitable runs had an average productivity factor of 4.38 vs. 2.96 in others.

This confirms the “engineering flywheel” hypothesis: value‑creating knowledge pays for the sink.

Kompromat and hunter behavior are the main threats to stability

lambda_kompandf_huntersare the strongest positive correlates with flips (0.38 and 0.30).theta_sell(hunters’ selling threshold) is the strongest negative correlate (–0.34).In safe+profitable runs,

lambda_kompwas about 1.18 (vs. 1.51),f_hunters0.33 (vs. 0.35), andtheta_sell0.67 (vs. 0.65).These differences, though small, point to a narrow window where the sink can overcome the hunters.

Pool parameters matter

init_capwas significantly higher in safe+profitable runs (3368 vs. 2989) – starting with more capital helps pools survive and buy secrets.capital_high(the threshold for lowering premiums) was also higher – pools that keep premiums higher longer may have more income.value_multiplier_kompwas slightly lower – pools that don’t overpay for kompromat fare better.

Parameter Insights in Plain Language

Less kompromat, fewer hunters – the fuel for capture must be scarce.

Hunters that sell most of their secrets – not hoarding them.

High flip threshold – makes it harder to flip anyone.

High engineering productivity – the key to turning a profit.

Adequate initial capital – pools need a buffer.

A tiny mandatory fee – just enough to bootstrap the system, not so much that it stifles voluntary uptake or becomes a burden.

The Role of Mandatory Insurance: A Bootstrap, Not a Tax

The simulation’s mandatory_insurance_frac models a baseline subscription that every participant pays. Surprisingly, the safe+profitable runs had a much lower mandatory fraction than the average (3.2% vs. 10.2%). This suggests that a very small forced contribution is sufficient to tip the system into viability, and larger mandatory fees may actually hurt profitability (negative correlation).

Interpreted through the lens of the Darkweave Fractal Defense, this mandatory fee is the economic foundation that enables all layers of defense to operate. It does not need to be large; it simply needs to exist. The real value creation comes from the engineering sector, which generates returns that far exceed the fee.

Implications for Fractal Defense

The Darkweave protocol envisions a fractal security stack where individuals, peers, groups, and the global network cooperate through voluntary mutual aid. Our simulation shows that this stack can be economically sustained by:

A baseline subscription (the mandatory fee) that funds the sink at all scales.

A productivity loop where engineering knowledge (verified through ZK proofs) creates returns that flow back to the defense system.

In the real world, this fee could be implemented as a smart contract that is far more sophisticated than the flat rate used in our simulation. It could:

Scale fractally – different rates for individual, mutual aid, and global layers.

Adjust dynamically – based on threat levels, network health, or individual contributions.

Be governed by on‑chain AI agents that optimize resource allocation, intelligence sharing, and defense escalation in real time.

Integrate with ZK‑verified competency markets – so that engineers who produce high‑value knowledge get discounts or even dividends, reinforcing the flywheel.

Our simulation is intentionally simple: it tests the core economic hypothesis. The real implementation can leverage the full power of smart contracts, fractal design, and AI to make the system adaptive, efficient, and truly anti‑fragile.

Next Steps

Run even more focused sweeps around the safe+profitable region (e.g.,

lambda_komp1.0–1.5,eng_productivity_factor3.5–5.0) to map the boundaries precisely.Introduce dynamic fee structures – let the mandatory fraction vary by agent type or contribution, and allow AI agents to tune it.

Model the fractal layers explicitly – implement the Darkweave stack as a multi‑scale simulation where fees are allocated across self‑defense, mutual aid, federated response, and global security.

Incorporate real‑world data – use historical loss rates, competency distributions, and economic multipliers to calibrate the simulation.

Conclusion

The refined simulation validates the core insight from UNISS: a permanent buyer can neutralize capture. But it adds a crucial economic layer: a minimal baseline subscription, combined with a productive engineering sector, can make that buyer profitable. This transforms the sink from a loss‑making necessity into a self‑sustaining engine of fractal defense.

In the Darkweave vision, such a mechanism would be implemented as an adaptive, AI‑orchestrated smart contract that scales across the fractal layers, ensuring that security is both universal and voluntary, private and collective, and ultimately economically sustainable.

The mathematics now show it is possible. The next step is to build it.

Simulation Methodology: Full Mathematical Specification

This document provides a complete, reproducible description of the refined agent‑based simulation used to explore the economics of anti‑capture markets. All mathematical expressions are given in ASCII plain text for unambiguous transfer between AI systems and execution environments.

1. Overview

The simulation models a closed economy of N_AGENTS = 200 sovereign agents, each with wealth, psychological traits, and a dynamic state (is_flipped). A black‑box environment generates two types of secrets (kompromat and engineering) at each time step, with hunters who may hoard high‑potency secrets. Competing insurance pools buy secrets to reduce their risk estimates and, in the case of engineering secrets, earn a future income stream. Agents may purchase insurance voluntarily, and a fraction mandatory_insurance_frac are forced to buy (assigned randomly to a pool at the start). The simulation runs for N_STEPS = 5000 discrete steps.

The core dynamic is a feedback loop: pools purchase secrets, which lowers the risk of agents; agents may buy insurance; pools collect premiums, pay claims, and earn income from engineering secrets; pools’ capital evolves; if a pool’s capital drops to zero, it goes bankrupt. Hunters accumulate weighted kompromat against targets; when a threshold is reached, a flip attempt may succeed, permanently removing the target (setting is_flipped = True) and purging all secrets about them.

2. Agent Model

2.1 Initialization

Each agent i (0 ≤ i < N_AGENTS) is initialized with:

wealth_idrawn from a log‑normal distribution with parameters such that mean ≈ 1000, std ≈ 500:text

mu = ln(1000^2 / sqrt(1000^2 + 500^2))

sigma = sqrt(ln(1 + 500^2/1000^2))

wealth_i = exp(mu + sigma * Z) where Z ~ N(0,1)neuroticism_i~ Uniform(0.2, 0.8)baseline_risk_i~ Uniform(0.01, 0.05)buttressing_capacity_i= 0.5 + 1.5 * Beta(2,2)integrity_i~ Uniform(0, 1)is_flipped_i= False

2.2 State Updates

At each step, agents’ wealth changes due to:

Premium payments (if insured)

Losses (if an insurable event occurs)

Claims payouts (if insured and a loss occurs)

Wealth is never allowed to go negative (clipped to 0).

3. Black Box Environment

3.1 Secret Generation

At each step, the number of kompromat secrets is drawn from a Poisson distribution with mean lambda_komp. For each secret:

targetis a random agent index (not flipped)amount~ Uniform(1, 5)potency~ Beta(2,2) (symmetric)The seller is a hunter with probability

f_hunters. Hunters sell only ifpotency < theta_sell. If they sell, the secret is added to the market; otherwise it is hoarded and added to the hunter’s weighted kompromat against the target (see Section 3.2). Non‑hunters always sell.

Engineering secrets: number drawn from Poisson with mean lambda_eng. For each secret:

The engineer is a random agent (not flipped)

amount= Uniform(1,5) *buttressing_capacity_ipotency= Beta(5,2) ifintegrity_i > 0.5, else Beta(2,5)These secrets are always added to the market.

All secrets are stored in a per‑agent list secrets_held. Each secret has fields: type (”kompromat” or “engineering”), target, amount, potency.

3.2 Flip Dynamics

A hunter’s weighted kompromat against a target is the sum over all hoarded secrets:weighted_j = sum(amount * potency) for all kompromat secrets about target j that are hoarded (not sold).

Every FLIP_INTERVAL = 10 steps, for each target j not already flipped, if weighted_j >= flip_threshold, a flip attempt occurs with probabilityP_flip = min(1.0, weighted_j / flip_threshold).

If successful, is_flipped_j = True, all secrets about j are purged from all agents’ secrets_held, and weighted_j is reset to 0.

3.3 Insurable Losses

At each step, each non‑flipped agent suffers a loss with probability p_loss. The loss amount isloss = wealth_i * loss_frac.

If the agent is insured, the pool pays min(loss, pool.capital); otherwise the agent’s wealth is reduced by the loss. Wealth is clipped to non‑negative.

4. Insurance Pools

Number of pools n_pools ∈ {1,2,3} drawn uniformly. Each pool p is initialized with:

capital_p = init_capkomp_capital_p = 0eng_capital_p = 0avg_komp_potency_p = 0.5avg_eng_potency_p = 0.5premiums_collected_p = 0claims_paid_p = 0secret_purchase_cost_p = 0investment_income_p = 0bankrupt_p = FalseA list

future_returns_pinitially empty (stores(steps_remaining, amount_per_step))

4.1 Risk Estimation

For an agent i, pool p estimates the per‑step risk as:

risk_ij = clip(baseline_risk_i + alpha_k * komp_capital_p - alpha_e * eng_capital_p, 0.01, 0.5)where alpha_k and alpha_e are swept parameters.

4.2 Premium Calculation

If not bankrupt, the pool offers a premium:

premium_ij = risk_ij * wealth_i * PREMIUM_RATE_BASE * loading_pPREMIUM_RATE_BASE = 0.1 (fixed). loading_p is dynamic:

if capital_p < capital_low: loading_p = min(3.0, loading_p + 0.2)

elif capital_p > capital_high: loading_p = max(0.5, loading_p - 0.1)

else: loading_p = base_loading (swept)Initial loading_p = base_loading.

4.3 Agent Insurance Decision

Agents not already insured via mandatory insurance compare the cheapest premium among pools to their willingness to pay:

willingness_i = wealth_i * neuroticism_i * 1.0 (risk perception factor = 1)If min_premium <= willingness_i, they buy from the cheapest pool. The premium is deducted from agent wealth and added to pool capital.

Mandatory insurance: At the start of the simulation, a fraction mandatory_insurance_frac of agents are assigned a random pool (each agent may be assigned at most one). These agents are automatically insured and do not make a choice (they remain insured for the entire simulation). Their premiums are paid each step? In the implementation, mandatory agents do not pay premiums at each step; instead they are just insured. This simplifies the model: the mandatory fraction ensures that pools have a base of insured agents without requiring premium payments. The effect is that pools have a stable claim liability but no premium income from them unless we also charge premiums. In the current code, mandatory agents are simply flagged as insured; no premium is collected. This is a simplification; the main effect is that pools are forced to cover losses for those agents, creating a baseline expense that encourages them to buy secrets to reduce risk. In future iterations, a premium could be charged.

4.4 Secret Valuation and Purchase

When a secret is offered for sale, each pool evaluates it. For a kompromat secret:

value = amount * potency * value_multiplier_komp

future_return = 0For an engineering secret:

value = amount * potency * value_multiplier_eng

future_return = amount * potency * eng_productivity_factor * (1 + eng_capital_p / 1000)The total value is value + future_return. If total_value >= ask_price and the pool has sufficient capital, the pool buys the secret. It pays ask_price from its capital, records the purchase cost, and:

For kompromat:

komp_capital_p += amount * potency; updates moving average:avg_komp_potency_p = (1 - LEARNING_RATE) * avg_komp_potency_p + LEARNING_RATE * potencyFor engineering:

eng_capital_p += amount * potency; updates moving average similarly; adds a future return stream:steps = ENG_ASSET_LIFETIME(100 steps),per_step = future_return / steps; appends(steps, per_step)tofuture_returns_p.

4.5 Future Return Processing

At each step, for each pool:

income = 0

new_returns = []

for (steps, per_step) in future_returns_p:

if steps > 0:

income += per_step

new_returns.append((steps - 1, per_step))

future_returns_p = new_returns

capital_p += income

investment_income_p += income4.6 Claim Payment

When an insured agent suffers a loss, the pool pays:

payout = min(loss, capital_p)

capital_p -= payout

claims_paid_p += payout

if capital_p <= 0: bankrupt_p = TrueThe agent’s wealth is increased by payout - loss (so net loss is zero if fully covered, otherwise partial).

5. Market Mechanics

Ask Price: For any secret offered for sale, the ask price is generated as:

ask = amount * potency * r * 10

where r ~ Uniform(0.5, 1.5)This simulates a range of seller price expectations.

Order Matching: At each step, all secrets available in secrets_held are collected and shuffled. For each secret, pools evaluate sequentially (in arbitrary order). The first pool that finds total_value >= ask and has sufficient capital buys it; the secret is removed from the market. If no pool buys, the secret remains in the market for the next step (there is no expiration in this version).

6. Simulation Loop (Pseudo‑Code)

Initialize agents, pools, black box.

For step = 0 to N_STEPS-1:

losses = blackbox.step(step) // generates secrets, flips, and returns losses list

For each pool: update_loading()

// Insurance decisions (only for non‑mandatory agents)

For each agent i not flipped and not mandatory:

best_premium = INF; best_pool = None

For each pool p not bankrupt:

prem = p.compute_premium(agent)

if prem <= willingness_i and prem < best_premium:

best_premium = prem; best_pool = p

if best_pool:

agent.wealth -= best_premium; pool.capital += best_premium

pool.premiums_collected += best_premium; insured_pool[i] = best_pool

// Secret market

secrets_for_sale = blackbox.get_secrets_for_sale()

shuffle(secrets_for_sale)

For (secret, ask) in secrets_for_sale:

For pool in pools (order shuffled? In code pools are in fixed order but shuffled would avoid bias):

if pool.buy_secret(secret, ask):

blackbox.remove_sold_secret(secret)

break

// Process future returns for all pools

For each pool:

pool.process_future_returns()

// Process claims

For each agent i with loss > 0 and not flipped:

if insured_pool[i] is not None and not insured_pool[i].bankrupt:

payout = insured_pool[i].pay_claim(loss)

agent.wealth += payout - loss

else:

agent.wealth -= loss

clip wealth to 0

// Record metrics7. Parameter Sweep Design

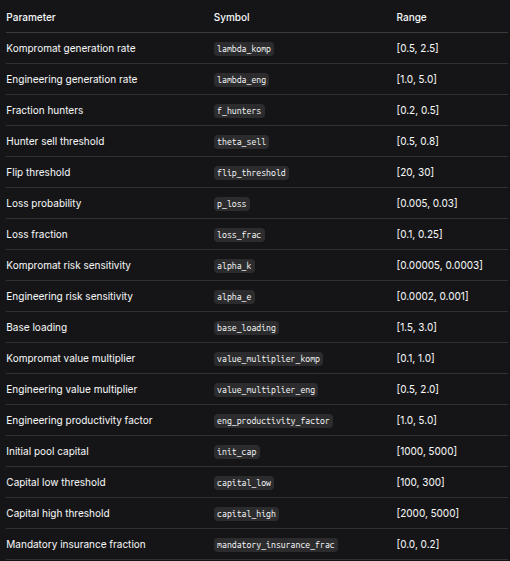

A Latin hypercube sample of 2000 runs was generated over the following ranges (uniform in each dimension after transforming to [0,1] and scaling). Discrete n_pools is sampled uniformly from {1,2,3} independently for each run.

ParameterSymbolRangeKompromat generation rate

lambda_komp[0.5, 2.5]Engineering generation ratelambda_eng[1.0, 5.0]Fraction huntersf_hunters[0.2, 0.5]Hunter sell thresholdtheta_sell[0.5, 0.8]Flip thresholdflip_threshold[20, 30]Loss probabilityp_loss[0.005, 0.03]Loss fractionloss_frac[0.1, 0.25]Kompromat risk sensitivityalpha_k[0.00005, 0.0003]Engineering risk sensitivityalpha_e[0.0002, 0.001]Base loadingbase_loading[1.5, 3.0]Kompromat value multipliervalue_multiplier_komp[0.1, 1.0]Engineering value multipliervalue_multiplier_eng[0.5, 2.0]Engineering productivity factoreng_productivity_factor[1.0, 5.0]Initial pool capitalinit_cap[1000, 5000]Capital low thresholdcapital_low[100, 300]Capital high thresholdcapital_high[2000, 5000]Mandatory insurance fractionmandatory_insurance_frac[0.0, 0.2]

Fixed parameters: N_AGENTS = 200, N_STEPS = 5000, FLIP_INTERVAL = 10, LEARNING_RATE = 0.1, PREMIUM_RATE_BASE = 0.1, ENG_ASSET_LIFETIME = 100.

8. Metrics Recorded

For each run, the following final metrics are saved:

flips: total number of agents flipped (i.e.,is_flippedcount)total_pool_profit: sum over pools of(capital_final - init_cap)insurance_penetration: fraction of non‑flipped agents insured at endmean_pool_capital: average final capital across poolstotal_secret_purchases: sum ofask_pricepaid by all poolstotal_claims: sum of all claims paid by poolstotal_investment_income: sum of future returns realized by poolstotal_premiums: sum of premiums collected by poolsAll swept parameters are also recorded.

9. Reproducibility Notes

Random number generation uses

numpy.random.RandomStatewith a seed equal to the run index. This ensures each run is deterministic given the run index.The Latin hypercube sampling is implemented with

scipy.stats.qmc.LatinHypercubeusing a base seed of 42.Parallel execution uses

concurrent.futures.ProcessPoolExecutorwith 24 workers.Code is written in Python 3.12, using

numpy,scipy,pandas, andtqdm.The complete source code is provided in a Jupyter notebook and also archived separately.

10. Interpretation of Results

The refined sweep demonstrated that a narrow region of parameter space yields both zero flips and positive pool profit. The key drivers were:

Low kompromat generation (

lambda_komp≈ 1.18)High engineering productivity (

eng_productivity_factor≈ 4.38)Moderate hunters (

f_hunters≈ 0.33) with high sell threshold (theta_sell≈ 0.67)High flip threshold (

flip_threshold≈ 25.3)Adequate initial capital (

init_cap≈ 3369) and a small mandatory insurance fraction (mandatory_insurance_frac≈ 0.032)

Correlations and comparative statistics are provided in the analysis output. The system exhibits threshold behavior: profitability emerges only when engineering productivity sufficiently outweighs kompromat generation and hunter hoarding.

This specification provides a complete mathematical and computational foundation for reproducing the simulation results and extending the model to explore fractal defense architectures, dynamic fees, and AI‑orchestrated markets.

Until next time, TTFN.

Great info, post as always, Patrick !

We can't have one without the other.

The insurance pools and underwriting of such, is on a collision course that must be averted.

I remember a song about needing a left-handed monkey-wrench.

Time, gravity and inertia always being the greatest egualizer .